ADVERTISER DISCLOSURE: The Frugal Tourist is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as MileValue.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All information about the American Express Schwab Platinum has been collected independently by The Frugal Tourist.

EDITORIAL DISCLOSURE: Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities.

As a sole proprietor, you may be wondering if you’re eligible for business credit cards that offer travel points or cash-back rewards.

The answer is yes!

Sole proprietors are not excluded from taking advantage of these valuable perks.

In fact, using a business credit card can help you build your credit score, manage your expenses, and earn rewards that you can use to reinvest in your business or even take a much-needed vacation.

In this article, I will provide some tips on how to answer a business credit card application so you can start earning travel points and cashback, which you can redeem for the vacation of your dreams.

Join Our Free Travel Miles & Points Facebook Group

Why Apply For Business Credit Cards?

As a frugal traveler, I have been leveraging business credit card sign-up bonuses to travel the world at a significant discount.

By and large, business credit cards provide generous welcome bonuses (usually between 50K to 150K points) that can be ultimately used to redeem for free flights and hotel stays.

Business cards have a very minimal impact on your personal credit scores and are relatively easy to get approved for.

In this article, you will learn about business credit cards and get tips on filling out two business credit card applications so you can confidently complete one yourself.

The examples provided in this blog post were application questions from the following banks:

- Chase Business Credit Card Application

- American Express Business Card Application

I Do Not Have a Company or an EIN. Am I Eligible for a Business Credit Card?

If you own a company or are a self-employed full-time contractor, applying for a business credit card should already be easy.

But for part-time side hustlers who occasionally moonlight, filling out a business credit card application can be incredibly unnerving.

I could imagine how it could get quite daunting to provide information, such as your company’s name and EIN (Employment Identification Number), when you do not have them.

It also does not help that there is a common misconception that seasonal side hustlers are not classified as business owners, thereby automatically disqualifying them from business credit cards altogether.

Nothing Can Be Further From The Truth

Regardless of the revenue, anyone who earns a profit from any type of venture is considered a sole proprietor and, therefore, eligible to apply for business credit cards.

In this post, I aim to demystify the business credit card application process so you can confidently answer the form even if you are a sole proprietor and do not have an EIN (Employer Identification Number).

Above all, I would like to increase your odds of getting approved so you can inch closer to your next bucket-list vacation.

Side Hustlers are Eligible to Apply for Business Credit Cards

Anyone who currently has a side hustle or is merely thinking of a future side hustle may be eligible to apply for a business credit card.

That’s right; you may be eligible even if your business is in its initial stages!

Simply put, your side hustle does not need to be completely off the ground yet—you can also qualify while conceptualizing it.

Generally speaking, though, having an existing side hustle, regardless of income, fundamentally makes you a more qualified candidate, but it is not a requirement. Hence, any start-up is eligible.

What Businesses Qualify As a Side Hustle?

Any Side Hustle is Considered a Business.

When I first applied for a business credit card over a decade ago, I was skeptical that I would qualify.

I only periodically ” sold” junk on eBay and Craiglist, and the income I received from it was inconsistent and barely enough to pay for gas.

When I got approved for my first-ever business card, I was beyond thrilled.

Do you mean I can get travel points to book business class tickets by selling random stuff online? Absolutely!

List of Popular Side Hustles

- buying and selling online (Facebook marketplace, Amazon, Etsy, eBay, etc.)

- tutoring

- driving for Uber/Lyft

- tour guide

- being an Airbnb host

- caregiving

- babysitting

- dog-walking

- instacarting

- door dashing

- coaching/consulting

- any manual labor you do on the side – plumbing, electrician, mowing the lawn, etc.

- having your own blog/podcast/YouTube channel

- having a rental property

- any freelance gig that yields a 1099 come tax time

- your side hustle!

In summary, you don’t need to own a multi-million dollar company to qualify for a business card.

Nor would you need to have a physical office either – your business address can be your primary residence.

In fact, you also don’t need to work in your business full-time. It can be part-time, seasonal, or a few hours throughout the year.

Any side hustle will do, regardless of the nature and structure of your venture.

As long as you are engaged in some form of activity to earn a profit, you can apply for a business credit card.

Income And Credit Scores

How Much Income Do I Need When Applying for Business Credit Cards?

When I started my side hustles over a decade ago, the income I generated from them was nothing to write home about.

I endured many years of floundering ventures until I got to where I am now.

Even though my business endeavors were fumbling then, that did not impact my eligibility to get approved for business cards.

So, I continued applying and traveling for free despite having numerous downturns.

The point is that “income” is not the only factor banks will consider before approving.

Instead, banks will most likely focus on your entire financial history to determine your viability. Thus, it is a recommended practice to cultivate a stellar credit score.

How About My Credit Card Utilization Rate?

The banks will also certainly assess your credit utilization rate, which is simply the ratio of your debt to the total credit you have.

The following formula calculates this ratio: “What You Owe” divided by “Your Total Credit.”

The lower your credit utilization rate is, the higher the likelihood of approval.

At any rate, as long as you have a side hustle, you could potentially get approved regardless of your current earnings.

In fact, you don’t even need to have a steady revenue stream.

Of course, who doesn’t wish for consistency in our income sources?

But if you are concerned that not earning enough could adversely affect your application, it generally wouldn’t.

Am I a Good Candidate for a Business Credit Card?

Since I value frugality and not frivolously spending on unnecessary expenses, I do not recommend applying for business credit cards if you are having a challenging time executing the following:

- Pay the bill on or before the due date

- Pay the bill in full

The goal is to fly for almost free. So, paying finance charges inherently defeats the purpose of this strategy.

Therefore, if you have existing consumer debt, pay it off before applying for business credit cards.

Alternatively, if you have difficulty adhering to paying your credit card balances altogether, then I strongly suggest bolstering your savings account first by employing these heavyweight saving strategies.

Once you possess this new frugality habit and have saved up a decent emergency fund, you are more than ready to sign up for business credit cards.

Remember, paying banks ridiculously high interest charges is never a good idea.

What Are The Chances That I Will Get Approved?

If this is your first business credit card application, you are more likely to not get instant approval.

But please do not worry; this is quite common.

Typically, banks require some time to evaluate your application and assess your financial history & credit score, especially if this is your first time applying for a business credit card.

At the end of the day, they will still be at the losing end if the consumer has a high risk of defaulting.

If your credit history shows that you are financially responsible, you will most likely receive an approval letter in the mail.

I cannot emphasize the importance of maintaining an immaculate credit score (740+).

Please reach out to us at the free Travel Miles and Points Facebook group if you have any questions about the business card application process.

Update: While Chase and Citi may not approve new business credit card applicants immediately, American Express seems to be relatively more lenient.

How Do I Answer a Business Credit Card Application as a Sole Proprietor?

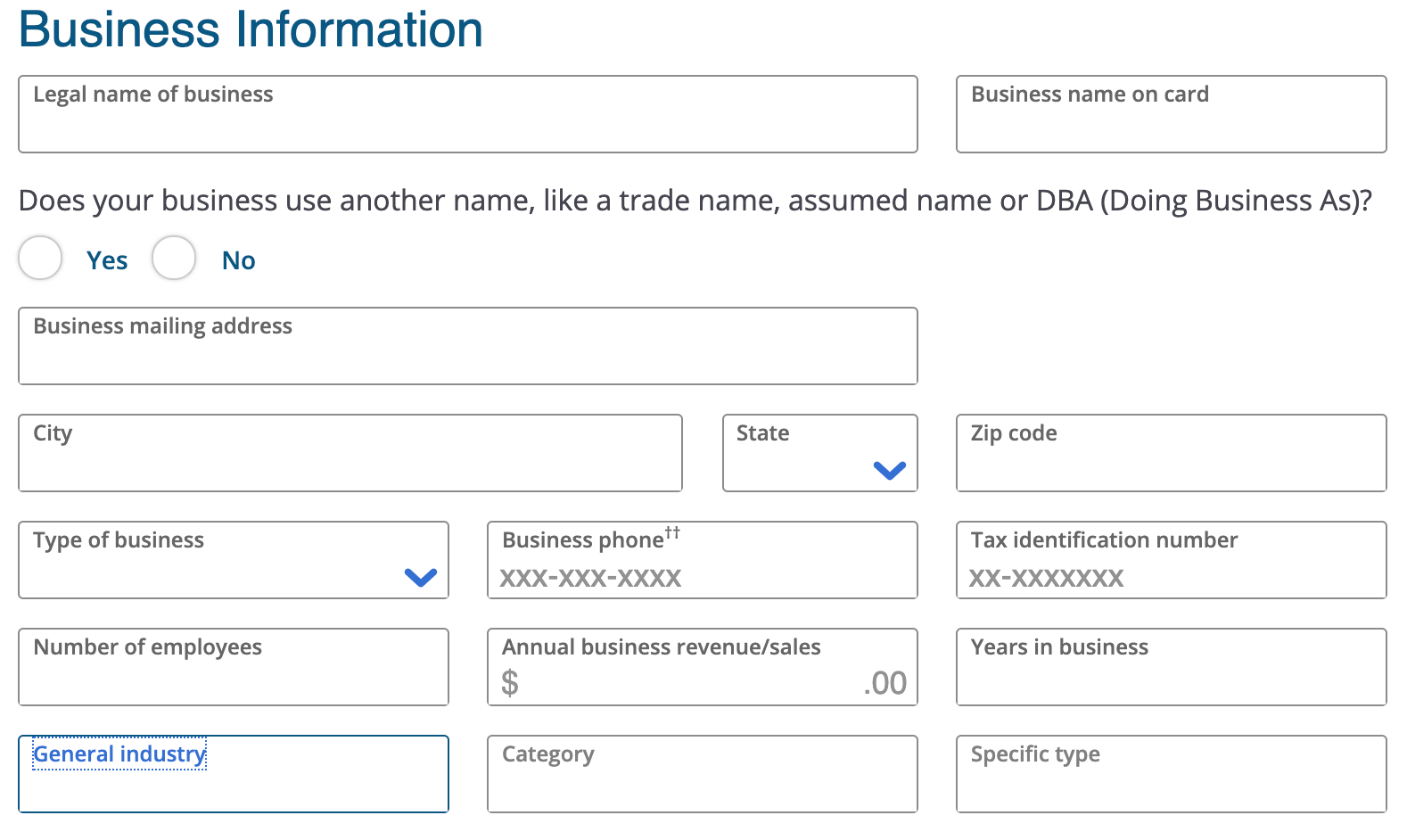

There are two components to a Business Credit Card Application.

- Business Information Section

- Personal Information Section

Rule Of Thumb: Be Truthful

Below are the typical questions included in a business credit card application and my cheat sheet on how to answer them.

The example below will illustrate how to answer a Chase Business Credit Card application.

This post will also provide an example of how to answer an American Express Business Credit Card application later.

Coming soon: Capital One Business Credit Card application

Chase Business Credit Card Application

Business Section of a Chase Business Credit Card Application

| Question | Answer |

|---|---|

| Legal Business Structure | Sole Proprietorship |

| Business Legal Name | Your Full Name (e.g. Kris Abad) |

| Desired Business Name on Card | Your Full Name |

| Indicate the date when you started to conceptualize your business. | No |

| Tax ID Type | Social Security Number (SSN) |

| Is Your Business’s Physical Address The Same As Your Personal Address? | Yes |

| Number of Employees (Enter the number of all additional employees, not including yourself. Enter “0” if you’re the only employee.) | 0 |

| Business Phone | Same as Personal |

| Business Established Date | Choose One/Select the Category of Your Particular Side Hustle. If your side hustle is Facebook Marketplace, then I would select “Retail: Automotive, Clothing, Food, Gas, Health, Home Goods.” |

| Annual Business Revenue | Estimated Annual Profit of your Business ($1000 or higher). |

| Business Category | Choose One/Select the Category of Your Particular Side Hustle. If your side hustle is Facebook Marketplace, I would select “Retail: Automotive, Clothing, Food, Gas, Health, Home Goods.” |

| Business Type | Choose any items on the drop-down menu. (Examples: Clothing, Home, etc.) |

| Business Sub-Type | Select from the drop-down. |

| NAICS Code | Leave blank |

| Estimated Monthly Spend | $50+ |

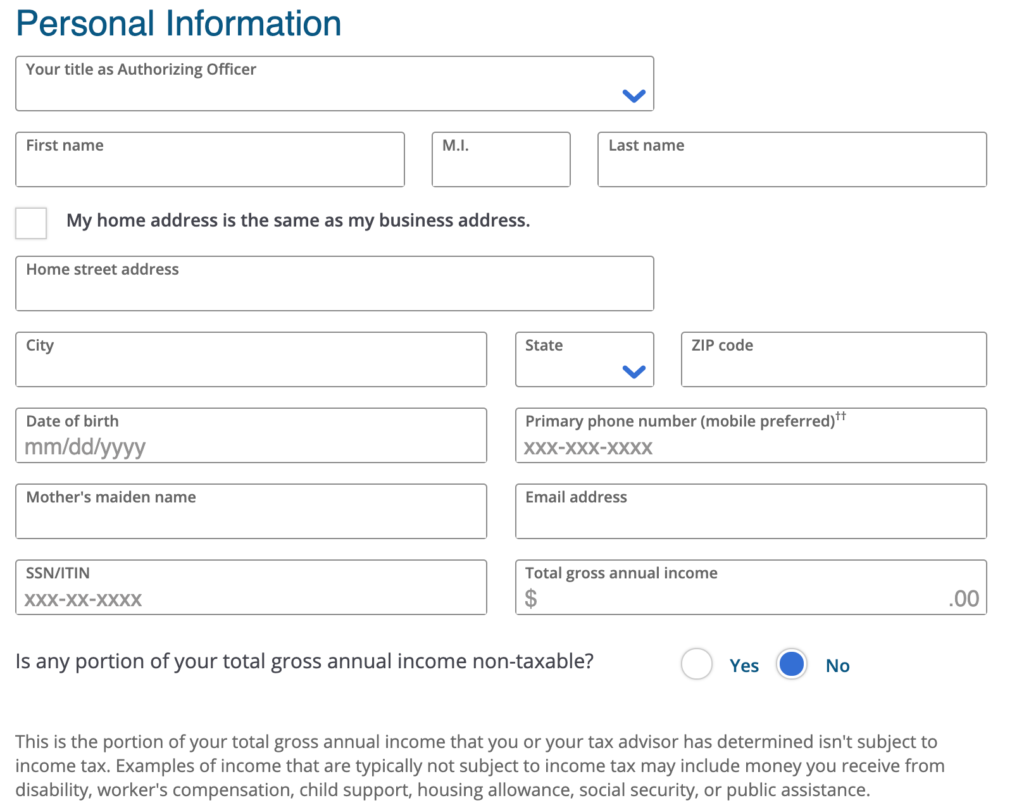

Personal Section of a Chase Business Credit Card Application

| Question | Answer |

|---|---|

| Authorizing Officer Title | Owner |

| First & Last Name | First & Last Name |

| Date of Birth | Your Date of Birth |

| Primary Phone Number | Mobile Phone |

| Mother’s Maiden Name | Your Mother’s Maiden Name |

| Email Address | Email Address |

| Tax ID Type | Social Security Number |

| Address Type | Domestic |

| Total Gross Annual Income | Your Annual Gross From All Revenue Streams (Full Time Job, Side Hustles, etc.) |

Before applying, I recommend that you read the entire blog post so you can determine your eligibility and know how to troubleshoot when denied.

Chase Business Credit Cards

| Credit Cards | Welcome Offer | Rewards |

|---|---|---|

| Chase Business Credit Cards | ||

| Ink Business Cash® Credit Card | Welcome Offer | Cashback |

| Ink Business Unlimited® Credit Card | Welcome Offer | Cashback |

| Ink Business Preferred® Credit Card | Welcome Offer | Travel Points |

| Ink Business Premier℠ Credit Card | Welcome Offer | Cashback |

| Co-Branded Business Credit Cards | ||

| IHG One Rewards Premier Business Credit Card | Welcome Offer | IHG |

| World of Hyatt Business Credit Card | Welcome Offer | Hyatt |

| United℠ Business Card | Welcome Offer | United |

| Southwest® Rapid Rewards® Performance Business Credit Card | Welcome Offer | Southwest |

| Southwest® Rapid Rewards® Premier Business Credit Card | Welcome Offer | Southwest |

Convert Chase Cash Back Into Travel Points

The Ink Business Cash and Ink Business Unlimited are advertised as cash-back cards.

Thankfully, there is a way to convert cashback from these cards into travel points (Chase Ultimate Rewards Points).

The post below will walk you through the steps on how to do this conversion.

Chase Bank’s 5/24 Rule

One important consideration when applying for Chase Cards includes the recommended Chase Ink Business Cards above.

Chase instantly rejects applications if you have applied and gotten approved for five personal credit cards in the past 24 months.

This policy is called the 5/24 rule.

This is an important rule to be familiar with when applying for Chase cards.

Even though your application is contingent upon your 5/24 status, business cards do not add to it, thankfully, since only personal cards affect your 5/24 standing.

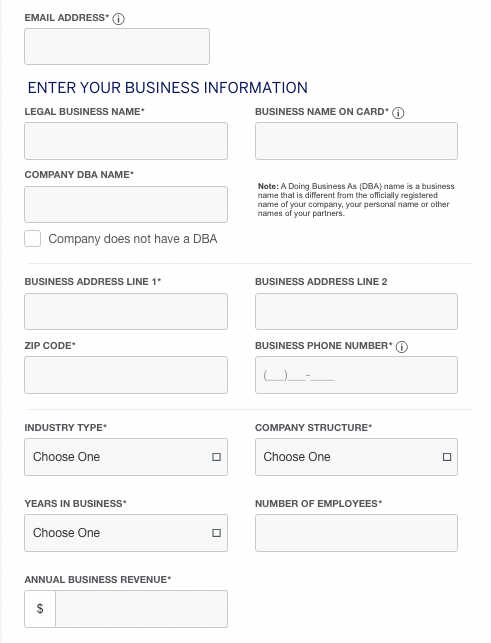

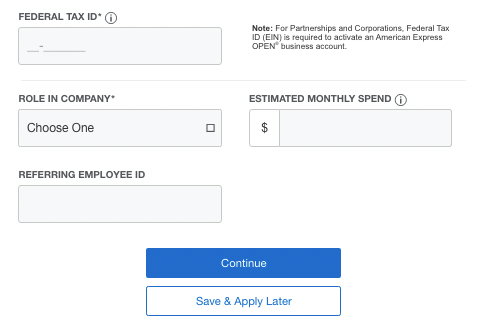

American Express Business Card Application

How to Answer an American Express Business Card Application

| Questions | Answers |

|---|---|

| Legal Business Name | Your Full Name (if Sole Proprietor) |

| Business Name on Card | Your Full Name (if Sole Proprietor) |

| Company DBA Name | None (Check Company does not have a DBA) |

| Business Address | Your Address |

| Business Phone Number | Your Phone Number |

| Industry Type | Choose One Retail Trade (if Facebook Marketplace) |

| Company Structure | Sole Proprietorship |

| Years in Business | At least one year (include the time you were conceptualizing the biz) |

| Number of Employees | One (1) if you are the only employee |

| Annual Business Revenue | At least $5,000 (estimated revenue for the next 12 months) |

| Federal Tax | Leave Blank for Sole Proprietors |

| Role in Company | Choose Any |

| Estimated Monthly Spend | At least $100 |

American Express Business Cards

| Business Cards | Welcome Offer | Rewards |

|---|---|---|

| American Express Business Cards | ||

| American Express® Business Gold Card | Welcome Offer | Travel Points |

| The Business Platinum Card® from American Express | Welcome Offer | Travel Points |

| The Blue Business® Plus Credit Card from American Express | Welcome Offer | Travel Points |

| Co-Branded Business Cards | ||

| Delta SkyMiles® Gold Business American Express Card | Welcome Offer | Delta |

| Delta SkyMiles® Platinum Business American Express Card | Welcome Offer | Delta |

| Marriott Bonvoy Business® American Express® Card | Welcome Offer | Marriott |

| The Hilton Honors American Express Business Card | Welcome Offer | Hilton |

How Do I Meet The Minimum Spend Requirement (MSR)?

What is MSR (“minimum spend requirement”)?

To receive the above cards’ bonus rewards, you must meet a certain minimum spending requirement within a specific time frame. Failing to complete these conditions will forfeit your reward.

What If I Do Not Have a Business? Start One!

Do not fret; you do have a couple of options.

As mentioned above, applying for a business card is possible if you are still in the beginning stages of planning for a business.

As with all businesses, we need initial capital to fund our “start-up” expenses, and sometimes, the funding source can come from a credit card. Banks are aware of this.

Consider applying for business cards if you plan to start a podcast or a dog-walking side job (or any of the examples above).

The sign-up bonuses can be truly rewarding.

Pro-Tip: Selling Stuff at Facebook Marketplace is an easy side hustle anyone can start anytime!

It also goes without saying that if the COVID-19 pandemic taught us something, the future is fundamentally unpredictable.

No one can foresee if our business will be a roaring success or an unfortunate letdown.

Neither the bank nor you can foretell that.

Thus, viability is not a determining factor in getting approved.

Alternatively, if you do not plan to have a business in the future, I recommend exploring personal travel credit cards.

Final Thoughts

I am a huge fan of lucrative credit card sign-up bonuses, so I try to take advantage of these offers whenever the opportunity arises.

Having a side hustle or a business not only multiplies your earning potential but also exponentially increases the variety of cards you can apply for, consequently propelling you closer to your next dream vacation.

With that said, a gentle reminder to only apply for credit cards that you can comfortably pay once your statement comes around.

Paying those hefty credit card fees is antithetical to the frugality principles I espouse in this blog.

I hope the actionable tips outlined in this post can help you acquire your first-ever business credit card.

Feel free to reach out anytime with questions!

Good luck!

ADVERTISER DISCLOSURE: The Frugal Tourist is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as MileValue.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All information about the American Express Schwab Platinum has been collected independently by The Frugal Tourist.

EDITORIAL DISCLOSURE: Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities.

USER-GENERATED CONTENT DISCLOSURE: The comments section below is not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved, or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all questions are answered.

Trackbacks/Pingbacks